Ar-Rahnu scheme means providing short term financing, fast, hassle free and riba free to the public by pawning his/her jewelry to banks or any pawnshop as a security. It is one of the micro-credit and financial instruments for low income earners seeking financial support or assistance to meet their fast working capital or personal necessities. Ar-Rahnu is relatively a new concept of pawn broking in Malaysia even though pawn broking dates is one of the earliest recorded lending transactions in history, back in the ancient times. The Ar-Rahnu contract’s purpose is to pledge the security of a debt and it is not meant for investment or profitable use. Therefore, if the security pledging for Ar-Rahnu is contracted for such purpose, the exploitation of such money-making use will be considered as usury. It is in line with the objective of Ar-Rahnu which is to allow individuals, small traders and poor to fulfill their financing needs without having to resort other expensive means such as money lenders, interest-based loans as well as less weighty financing by acting as a source of capital to the small business, financing educational needs and helper to develop agricultural and village industries. Hence, the purpose of conducting this research is to determine whether the internal regulation made by those institutions is enough to protect both parties involved in case of dispute occurs or a specific law needs to be implemented and enforced. In consequence with research objective, qualitative analysis through in depth interview has been done with few of Ar-Rahnu implementer both banks and non-banks institutions. Based on the findings, there are not many issues that appear on those institutions of the Ar-Rahnu scheme but it is advised that specific law for Ar-Rahnu is implemented as this scheme grows rapidly due to the rise of awareness within the Malaysian community.

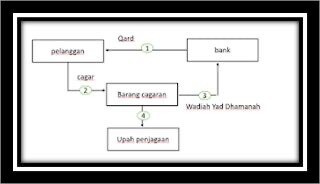

Modus operandi of Al-Rahn Financing Products

The figure above shows the structure of al-rahn products applied in Islamic banking that offers al-rahn products. Among them are Bank Kerjasama Rakyat Berhad (Bank Rakyat), Bank Islam Malaysia Berhad (BIMB), Bank Muamalat Malaysia Berhad (BMMB), Coopbank Pertama, Agrobank and Affin Islamic Bank. All Islamic Banks that offer al-rahn products used to use the same Shariah concept, namely rahn, qard, ujrah and wadiah yad dhamanah.

First, the customer pledges the pledged assets i.e. jewelry or goods to the bank with the conditions set by the bank for the purpose of loan collateral (al-rahn). The bank will make an assessment on the quality and purity of the gold. Based on this assessment, the Bank will determine the loan that the customer is eligible to receive. For example, 70% of the value of the pledged gold. Second, the loan (qard) will be given to the customer in the short term after the mortgage declaration letter is signed. Third, banks are responsible for storing and guaranteeing (wadi'ah yad dhamanah) on the mortgaged goods so that they are safe and secure. Lastly, the customer will pay the loan and the fee (ujrah) charged on the security guarantee and storage of the pawn on the customer according to the terms of the agreement (BNM, 2019).